Disclaimer: This content is for informational purposes only and should not be taken as financial or investment advice. Always follow your local laws and your exchange’s terms of service when using a VPN.

Cryptocurrencies offer more privacy than traditional banking, but your connection can still expose your data. Whether you’re trading, logging into your wallet, or checking prices on a crypto exchange, unsecured or public networks can make you more visible to trackers and potential attackers.

A VPN adds an extra layer of security as it encrypts your traffic and hides your IP address, helping keep your browsing and activity more private. While most VPNs offer various privacy features, choosing one made specifically for cryptocurrency makes sure you get the right combination of speed, protection, and crypto-friendly options. Here’s how you can use a cryptocurrency VPN to add a layer of protection to your data.

A VPN helps protect your privacy online, especially on untrusted networks. However, it doesn’t make you 100% anonymous or guarantee protection against fraud, scams, platform actions, or financial loss. Also, keep in mind that not all crypto exchanges allow the use of VPN apps. Always follow local laws and your exchange’s terms.

What Is a Crypto VPN?

A crypto VPN is a tool that protects your traffic in transit and masks your IP address. When you connect through a VPN, your internet data is encrypted between your device and the VPN server. Masking your IP address also reduces IP-based profiling and helps keep your IP address separate from your trading sessions. This helps keep your connection secure when trading on shared or public networks, at home, or while traveling.

Some VPNs signal their privacy focus through how they accept payments. In addition to cards and PayPal, some support crypto payments, so you can sign up without sharing card details. For example, CyberGhost VPN supports Bitcoin, which is useful if you prefer to keep billing separate from your everyday financial accounts.

Keep in mind that while a VPN makes your data more private, it doesn’t make you anonymous to services you sign in to. Once you log in to an exchange or hosted wallet, the platform can link your actions with your account, even if you’re on a VPN. KYC/AML exchanges will still log your activity under your identity. A VPN also doesn’t hide on-chain activity, as public blockchains record transactions by design. That’s why it’s crucial to pair a VPN with good account hygiene: use a password manager, create unique passwords, enable 2FA authentication, and keep your software up to date.

How a VPN Helps Protect Your Privacy on Crypto Platforms

A VPN does more than “turn on encryption.” It adds a layer of privacy to your online activity, helping limit who can track your browsing and reducing exposure to fake and malicious recovery or login pages.

Keep Your Crypto Activity Private with Encryption

When you access a crypto exchange or your wallet, your internet traffic can be intercepted. This is especially true for public Wi-Fi networks, where the risk of exposure is higher. Shared networks are often poorly secured, making it easier for someone on the same network to observe your internet traffic.

A VPN helps you regain privacy online through encryption. It creates a secure connection between your device and the VPN server, so others on the network can’t read your traffic. That helps keep exchange logins, session cookies, and browsing activity away from prying eyes. The exchange can still see your activity once you’re signed in. However, third parties and your internet provider will see only that you’re connected to a VPN server.

Avoid Being Tracked Online

Connecting to a VPN replaces your IP address with one from the VPN server, making it harder for websites and apps to link your online activity to your physical location. This reduces profiling and tracking based on your network identity.

This means you can keep your internet connection private even while traveling or using networks you don’t fully trust, like airport or hotel Wi-Fi. A VPN will protect your logins, session cookies, and other information from people on the same network. However, not all crypto exchanges allow the use of VPNs. Always check their terms of use before using a VPN IP address to access them.

Avoid Online Scams That Target Your Coins

Phishing websites and malware are a major threat to crypto holders. Scammers are known to create fake crypto exchange logins or wallet recovery pages to steal credentials. These sites can appear in search results, online ads, or suspicious links sent via email or messaging apps.

Some VPNs help reduce this risk by including ad and tracker blockers, along with databases of known malicious domains. If you try to visit one of these flagged sites, the VPN may block the connection or warn you before the malicious page loads.

How to Choose a VPN for Crypto Privacy

With numerous VPNs available on the market, selecting the right one for protecting your crypto activity can feel overwhelming. To enhance your connection privacy, a VPN should deliver:

- Strong encryption: Pick a VPN that uses modern encryption, like 256-bit AES, to keep your internet connection secure and make it harder for others to intercept your traffic.

- No-logs policy: Choose a cryptocurrency VPN with an audited no-logs policy to ensure it doesn’t collect or store data about your online activity.

- Wide server network: Go for a VPN with servers in as many countries as possible, as using a nearby VPN server gets you the fastest possible speed.

- Leak protection: Make sure your VPN includes DNS, IPv6, and WebRTC leak protection. This can prevent accidentally exposing your real IP address.

- Kill switch: Ensure your VPN has a kill switch that cuts your web access if your signal suddenly drops and keeps you offline until your connection is stable again.

- Fast and secure protocols: Look for VPNs that support WireGuard® or OpenVPN. They deliver strong data privacy while maintaining quick speeds.

- Secure payment methods: Select a VPN provider that accepts payments in Bitcoin or other cryptocurrencies. That way, you can subscribe without providing your card details, adding an extra layer of privacy.

- Reliable customer support: Get fast help when you need it. The most reliable VPNs offer 24/7 live chat and email customer support.

- Budget-friendly price: Find a VPN that fits your budget. Reputable VPNs typically offer a money-back guarantee, so you can test the service risk-free before committing.

CyberGhost VPN can keep your crypto activity private with advanced encryption, protocols like WireGuard® and OpenVPN, and servers in key locations worldwide. Built-in ad and tracker blocker adds another layer of safety, and a 45-day money-back guarantee lets you try it risk-free.

How to Pay for a VPN with Bitcoin and Other Crypto

Paying with crypto can offer more privacy than traditional payment methods, because it doesn’t require linking your credit card to your account. We’ll use CyberGhost VPN as an example of how to sign up with crypto.

- Visit your chosen VPN’s website and open its pricing page. You can usually do it by clicking on buttons like Get It Now, Buy a VPN, Pricing, etc.

- Check out available plans. Pick a subscription and click Continue to Checkout. CyberGhost VPN offers significant savings when you opt for a long-term plan.

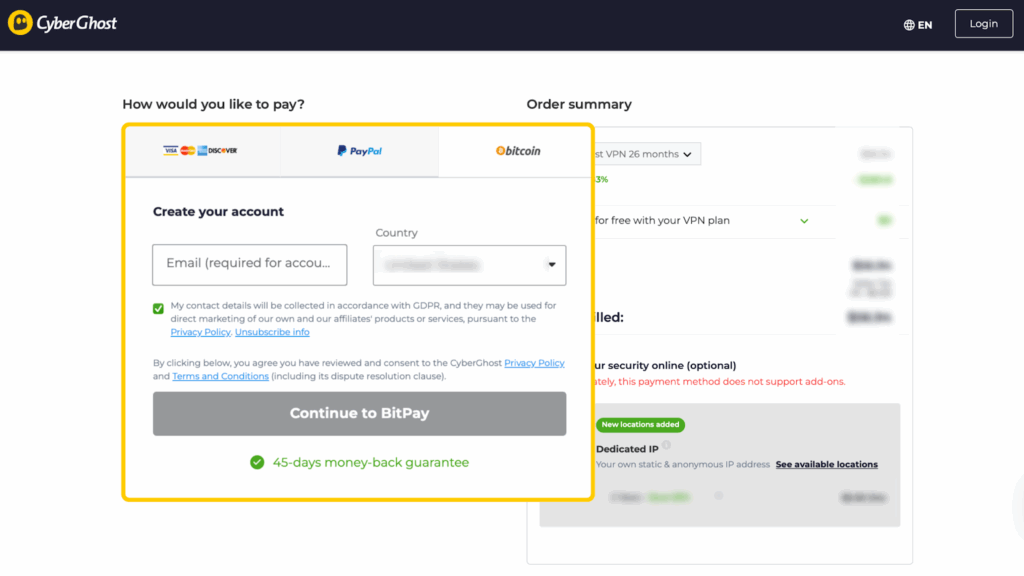

- Input your details, such as your email address. Pick Bitcoin or any other cryptocurrency. Then, pay for your subscription using the Continue to BitPay button. Follow the prompts on the cryptocurrency payment page to complete and confirm your purchase.

Best Practices for Using a Crypto VPN

To get the most out of your cryptocurrency VPN, you should:

- Stick to proven VPN protocols: WireGuard®, OpenVPN, and IKEv2 are all widely used, secure VPN protocols that deliver strong online privacy. IKEv2 is especially reliable on mobile.

- Use a kill switch to avoid data leaks: Ensure your VPN has a kill switch enabled, which you can do through the app’s settings. Some VPNs, like CyberGhost VPN, have this feature turned on by default.

- Avoid using public Wi-Fi without a VPN: Activate your VPN before connecting to public Wi-Fi networks. That way, you’ll keep your data protected from potential snoops.

- Switch servers to improve speed and regain access: Go with a different server if you experience slow speeds or connectivity issues.

Why Crypto Payments Are Risky

Cryptocurrencies offer more privacy than traditional payment methods, but they’re not bulletproof. Here are the main risks to be aware of when making crypto payments online:

- Exposing your wallet on public Wi-Fi: Cybercriminals can create fake Wi-Fi hotspots with names like “Free Airport Wi-Fi” or intercept traffic on unsecured networks. If you log in to your wallet or exchange without encryption, they could capture your private keys, recovery phrases, or transaction details.

- Revealing your activity to your ISP: Your internet provider can see which crypto services you use and how often. That metadata may be stored, depending on company policy or local regulations. It might also be used for analytics and shared if the law permits it. In rare cases, it could even be leaked in a breach.

- Facing location-based restrictions: Local networks, like those at workplaces, schools, or public institutions, can block access to trading platforms. This can stop you from managing your account when you need to.

- Allowing exchanges to track your behavior: Exchanges can log your IP address and link it to your account activity. Over time, this creates a profile of your trading patterns, transaction amounts, and login times. This data can be analyzed, stored, or even shared with marketing partners or data analytics firms.

Use a VPN as a Part of Responsible Crypto Practices

Using a VPN for crypto doesn’t make you 100% invisible online, but it adds privacy and security when you interact with crypto-related services. Whether you’re managing your wallet, reviewing DeFi dashboards, or checking market data on hotel Wi-Fi, a VPN helps protect your traffic from prying eyes.

That’s where a trusted VPN like CyberGhost VPN comes in. It offers 256-bit AES encryption, a strict no-logs policy, and powerful data leak protection. You can also pay for your subscription more privately using cryptocurrency if you don’t want to use your bank card. Lastly, CyberGhost VPN has a 45-day money-back guarantee on long-term plans. If it doesn’t fit your needs, you can get a full refund.

FAQ

Should you use a VPN for crypto?

Yes, using a VPN can help protect your privacy when managing crypto accounts. Activities like logging in to wallets or exchanges involve sensitive information that could be exposed on untrusted networks. Using a VPN masks your IP address, which hides your physical location and identity. It also encrypts your traffic, making it unreadable to anyone trying to intercept it.

Which VPN location is best for crypto?

The best VPN location is usually the one closest to you. A nearby server gives you faster speeds and a more stable connection.

Most VPNs automatically pick the best server for your needs. CyberGhost VPN covers 100 countries and lets you auto-connect to a nearby, low-load server that delivers fast speeds and stable performance.

Is it legal to use a VPN for crypto trading?

In most countries, using a VPN is legal. However, laws about VPN use and crypto platforms differ by region. Always check your local regulations and the exchange’s Terms of Use before connecting. Some platforms may restrict or ban VPN connections, which could lead to account limitations if used in violation of their rules.

What is the best VPN for mining crypto?

Crypto mining requires a stable and fast internet connection. If you use a VPN while mining, pick one with stable servers and strong privacy protections so your connection isn’t interrupted or monitored.

CyberGhost VPN provides unlimited bandwidth, 256-bit encryption, and a strict no-logs policy for dependable online privacy.

Can a VPN protect my crypto transactions?

A VPN protects your connection, but not the blockchain or your wallet. It helps secure the path between your device and the website you’re using, which keeps your network traffic private from third parties, ISPs, or public Wi-Fi snoops. Always combine a VPN with secure wallets and two-factor authentication for deeper protection.

Will a VPN help bypass local restrictions on crypto?

A VPN can protect your privacy on restricted or public networks, but using it to bypass regional laws or platform restrictions may violate terms or regulations. Always comply with local laws and your exchange’s policies.

Can a VPN prevent tracking by crypto platforms or governments?

A VPN can make tracking more difficult by hiding your real IP address and encrypting your traffic. However, it doesn’t make you anonymous to platforms you log in to or to blockchain networks that record transactions publicly.

Does using a VPN reduce the risk of phishing in crypto trading?

Yes, a VPN can reduce the risk of phishing in crypto trading. Some VPNs, including CyberGhost VPN, can block access to malicious sites even before they load. This helps reduce exposure to phishing and scam pages. However, you also need to be careful about the links you click on, especially if you receive them via e-mail.

Can I use a VPN to create multiple crypto exchange platforms?

Most crypto exchanges prohibit creating multiple accounts, and doing so can lead to suspension or a permanent ban. Using a VPN doesn’t change or bypass those rules. Always follow the platform’s Terms of Use to avoid penalties or bans.

Is it safe to access my crypto wallet over public Wi-Fi with a VPN?

Yes, using a VPN can make public Wi-Fi safer by encrypting your connection and masking your IP address, which helps reduce (not eliminate) the risk of interception. Avoid sensitive actions on unsafe networks when possible.

Can exchanges detect or ban VPN users?

Yes, exchanges can detect VPN connections and may restrict or ban them if their Terms of Service prohibit VPN access. Always review the platform’s policies before connecting through a VPN to avoid account issues.

Leave a comment

Skyy tracker

Posted on 14/03/2022 at 12:10

very good information about crypto tokens

Adina Ailoaiei

Posted on 14/03/2022 at 16:34

Glad to hear you enjoyed reading, Ghostie.